What a week it was, as we came into Monday morning with stocks down significantly over worries about Chinese AI-based company DeepSeek. We will discuss that more below, but the bottom line is despite the large losses we saw in large technology names on Monday, last week really held up quite well overall.

So Goes January, Goes the Year

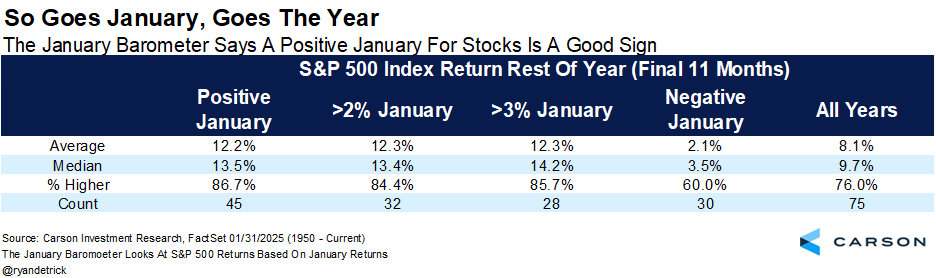

An effect widely known as the January Barometer looks at how the S&P 500 does in January and what it may mean for the next 11 months. It is known by the saying, ‘So goes January, goes the year’ in the media. The late Yale Hirsch first presented the phenomenon in Almanac Trader 1972. Today the Almanac is carried on by Yale’s son Jeff. We’ve followed Jeff’s work for years, and we believe the work they do is some of the best in the industry on market seasonality, calendar effects, and many other indicators.

Let’s look at the January Barometer. For starters, three years ago we saw the S&P 500 lower in January and it was followed by a vicious bear market. Then the past two years stocks were higher in January and we saw back-to-back 20% years.

Historically, when the first month was positive for the S&P 500, the rest of the year was up 12.3% on average and higher 86.7% of the time. And when that first month was lower? It was up about 2.1% on average and higher only 60% of the time. Compare this with your average year’s final 11 months, up an average of 8.1% and higher 76.0% of the time, so clearly the solid start to ’25 could be a positive for the bulls. Lest you fear January has been too strong, a good start to January tends to see strong gains the rest of the year as well, as we discuss below.

Here’s another way of showing what tends to happen based on whether January was higher or lower. We know markets trend, but my oh my, what that first month does can really pick the direction for the full year.

January is now in the books, and the S&P 500 was up well over 2% during the year’s opening month. That may also be a very good sign. Below we show all the times the first month of a new year gained at least 2% and you can see that continued outperformance is perfectly normal. The full year had and average gain of 18.4% and was higher nearly 88% of the time, which should have bulls smiling.

The Fed Hits the Snooze Button, but That Poses Problems

A somewhat sleepy Federal Reserve meeting received less attention than usual this week, even more so sandwiched between the DeepSeek news at the start of the week and tariff talk at the end of the week. But the path the Fed takes is still important, and over time too much caution about lowering rates could become a problem.

The Federal Reserve’s (Fed) January 2025 meeting held no surprises. They maintained policy rates within the 4.25-4.50% range and continued to trim their bond portfolio, as expected. However, their official statement did see a small, but notable, change. They did highlight that the unemployment rate has stabilized at low levels, but inflation remains “somewhat elevated.” By itself, this would indicate the Fed is hitting the snooze button on rate cuts, and the pause may last for a while. Fed Chair Jerome Powell’s response to a question about the possibility of a rate cut at their next meeting in March was that they’re not in a hurry to adjust their policy stance.

Markets are now expecting the Fed’s policy rate to be close to 3.9% at the end of 2025, implying two rate cuts in 2025 (each worth 0.25%-points), although that may change this week as the market absorbs the impact of newly announced tariffs. As of Thursday, the first hike is not expected before June. This is consistent with the Fed’s own projections from their December meeting, where they projected a couple of cuts in 2025. As you can see in the chart below, expectations have shifted in a big way from last September, when markets expected the fed funds rate to hit 2.8% at the end of 2025. The difference is that we’ve gotten a string of strong economic data since then, resulting in fading recession fears (and fewer rate cuts being priced in as a result).

Still, Powell’s Quite Optimistic About the Inflation Outlook

Powell sounded quite positive about the inflation picture. In fact, he explicitly backed away from the inflation language in the statement, saying it was mostly about “cleaning up the language.” He noted that the inflation numbers a year ago (in Q1 2024) were quite strong (remember that scare?), and that’s setting upcoming Q1 2025 for better year-over-year inflation readings due to positive “base effects.” This assumes we get benign monthly data over the next few months, akin to the positive data we got in December, which may be likely if shelter inflation continues to decelerate. At the same time, Powell does want to see the actual data evolve as they expect before moving. Hence the pause.

Powell also noted that the policy rate is still “meaningfully restrictive,” though less restrictive than before they started cutting rates in September. He sounded confident that the labor market is solid, but went on to say that they don’t want it to cool further. He pointed out that if you have a job, things are good. But if you don’t, it’s harder to find a job. And they don’t intend to make it even harder than it already is, at least not as a result of overly restrictive policy. This implies that any further weakening of labor market data should see them cutting rates earlier than expected.

They’re Clearly Worried About Trump Administration Policies

Powell’s positive inflation outlook, and desire not to cool the labor market further, begs the question: “Why not lower rates if they believe rates are meaningfully restrictive?” The short answer: rising inflation uncertainty. This was apparent in their December projection, and Powell more explicitly admitted to the reason in his press conference.

He said there is elevated uncertainty due to significant policy shifts, across four areas: tariffs, immigration restrictions, fiscal policy (more deficits), and regulatory policy. He admitted that they do need to see what the actual policy will be before estimating the economic impact, let alone determining the appropriate policy. But for now, the uncertainty is why they’re pausing, and the weekend announcement of potential tariffs on Canada, Mexico, and China, validate that outlook

A Pause Is NOT Status Quo; It Can Hurt

An extended pause is far from a benign policy choice. If inflation continues to pull back, as Powell himself expects, doing nothing would mean policy is actually getting tighter. This is going to have an adverse impact on rate-sensitive sectors of the economy, like housing and business investment (outside of AI-driven capex, where other factors like the fear of being left behind will drive more investment).

Elevated rates can also keep the dollar stronger, and that poses risks of its own. In particular, it hurts US exports, which is exactly what happened in the fourth quarter of 2024. The dollar index rose close to 8% over the quarter, and nominal goods exports pulled back at an annualized pace of 15%, while imports rose 10% annualized. Remember, a stronger dollar makes exports more expensive and imports cheaper. We wrote about this in our 2025 Outlook, when discussing potential threats to the economy.

The latest GDP growth numbers underline the risk of elevated rates, and a strong dollar. Real GDP growth clocked in at 2.3% for Q4 2024, a tad below expectations but still a solid reading and along trend. Consumption was strong once again, contributing 2.8%-points to Q4 GDP growth. Consumption rose 4.2% in Q4, accelerating from the 3.7% increase in Q3. Government spending also provided a 0.4%-point boost.

However, a lot of this strength was offset by investment spending, which pulled GDP down by 1%-point. A chunk of this was due to falling inventories, which tend to be volatile. More worryingly, fixed nonresidential investment, i.e. business investment, fell 2.2%, driven by an 8% drop in equipment spending and a 2% decline in investment into structures like manufacturing facilities and other buildings. Goods exports pulled back 5%, pulling GDP growth down by 0.4%-points. It was offset by services exports (mostly on the back of foreigners travelling to the US, which counts as a “service export”). Residential investment (housing) did make a 0.2%-point contribution to GDP growth in Q4, rising over 5%, but if mortgage rates stay close to 7%, that’s likely to become a drag.

All this to say, don’t let anyone tell you that elevated rates are not having a significant impact on the economy because headline growth is still humming. Key areas of the economy like investment and manufacturing exports are being hit due to elevated rates and a strong dollar. And there’s unlikely to be a boost from the housing sector either. If this continues, it could be the difference between 3% GDP growth versus 2% GDP growth.

Ultimately, Fed policy is going to depend on how the inflation data evolves, but also some clarity on policies coming from other side of D.C. Of course, if we see a deterioration in labor market conditions, we’ll likely see rate cuts sooner rather than later — but bad news is not something to root for (we’re consistently in the camp that good news is good news and bad news is bad news).

A Quick Take on DeepSeek

DeepSeek, a small Chinese artificial Intelligence (AI) startup, shook the AI world and markets the previous weekend after it released an AI model that appears to be as powerful as the existing ones, but trained at a fraction of the computing cost.

Until now, it looked like there would just be a handful of mega tech companies able to compete in the AI space: Microsoft-backed OpenAI (with ChatGPT), Alphabet (Gemini), and Amazon-backed Anthropic (Claude). The thinking was that only these companies had the immense technological and financial resources required. And subsequently, they would be able to monetize AI by charging users who wanted to use these proprietary, “closed source” AI platforms.

Well, DeepSeek just upended this.

The good news is that costs are likely going to be much lower for AI broadly, which is likely to pull in a lot more users. But one person’s spending is another person’s revenue (and profits). So, falling prices means companies providing AI infrastructure could potentially lose out.

Who and What Is DeepSeek?

DeepSeek was founded by a quantitative trading firm in China, one of China’s largest (they had $15 billion of assets in 2015, but this dropped to $8 billion by 2021). The founder of the trading firm, Liang Wenfeng, went into AI research two years ago in May 2023 — apparently with 10,000 NVIDIA chips they had acquired by 2021, before export controls were imposed by the US. They also pulled together the smartest young Ph.D.s across China’s top universities.

On January 20th, DeepSeek released DeepSeek-R1, a significantly more advanced reasoning model than its previous AI releases. The tech was the equal of competing AI across most major benchmarks. What made a large impression was innovative AI training methods that dramatically reduced the cost of training the AI. That is what sent US investors into panic, albeit only after digesting the information over the weekend.

Some highlights of DeepSeek

- It’s open source, with the goal of eventually giving everyone access to Artificial General Intelligence (AGI). They’re the only advanced AI team releasing cutting-edge research.

- The chatbot is free, with no ads, and it appears to be as good as the other chatbots.

- It allows you to see how it’s “thinking” as it gives you an answer, which helps you understand, and trust, the answer more. It also helps you tailor your queries and get to better results.

- The API pricing is lot lower than competitors. The R1 API costs $0.55 per million input tokens (versus $15 for ChatGPT) and $2.19 per million output tokens ($60 for ChatGPT).

What’s Next?

At the end of the day, you still want to have more chips rather than less, since it’ll allow for faster utilization and inference. Also, the wider use case of AI, as costs plunge, could lead to more demand. This is called as “Jevon’s Paradox”. When technology advances, it makes a resource much more efficient to use. But as the cost of the resource drops, demand increases, causing resource use to increase.

In line with that, what could end up happening is even more capex spending on AI, including on chips. In which case stock prices for chip companies that got hammered should recover, although the timing of demand could be different. But at this point, it’s likely too early to tell.

While the consequences for companies that provide AI infrastructure are more uncertain, there are also potential benefits for companies that are heavy users of AI, such as Apple, Amazon, and Meta, and smaller firms as well, which will likely benefit from the lower cost.

Focus On the Big Picture

Manufacturing is not a big part of the US economy. But China could be coming for US tech now. DeepSeek’s advances shows that China’s technological capabilities are a threat to US technology companies. And tech is an important industry for the US, not least because it matters for the stock market (more so because of current levels of concentration), and household balance sheets, which have strengthened partly on the back of stock market gains.

But US companies are not out of the game. Not by a longshot. As we mentioned earlier, you’d still rather have more chips than less. Keep in mind that there’s also a lot of research and development always going on at US companies and we don’t know the full extent of their AI advances. OpenAI and Google may not have released their “latest and greatest” models to the public.

A lot of the focus right now is on the winners and losers within the context of DeepSeek’s release. That’s a tough game to play, and thankfully one that we don’t really have to — the market will figure it out. The big picture is that AI is now going to diffuse into the economy much faster, thanks to lower cost. If anything, US companies are likely to ramp up spending on AI even more. That’s ultimately going to be a good thing for the economy, and productivity too.

Even before the DeepSeek news that led to last Monday’s selloff, there was a good case to be made for diversifying within equities, into areas like mid/small cap stocks and sectors outside tech, to reduce concentration risk. We wrote in our 2025 Outlook that we expect the bull market to broaden out this year based on the fundamentals of the economy and policy opportunities. Our view was that there’s good reason to diversify outside of the technology sector even prior to this latest news (note we’re neutral on tech, not underweight). There’s nothing that’s changed that outlook, and if anything, what’s happened this week has perhaps solidified it.

At the same time, don’t be surprised if there’s volatility as investors grapple with shifting dynamics, perhaps even more so given the tariff announcements over the weekend. One of our favorite charts shows the historical frequency of different levels of S&P 500 declines in an average calendar year. Declines of 3% are garden variety. We average 7.2 of those a year, which means that we’re more likely than not to see one in any given month. A mild correction of 5% or more occurs a little more than three times a year. Even a 10% “correction” typically occurs at least once a year, though we haven’t experienced one of those for over fourteen months now. Pullbacks are par for the course when it comes to investing, even though the narratives around the cause of those declines are always different. Just something to keep in mind as we get a lot of scary news headlines over the following week.

This newsletter was written and produced by CWM, LLC. Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The views stated in this letter are not necessarily the opinion of any other named entity and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

S&P 500 – A capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The NASDAQ 100 Index is a stock index of the 100 largest companies by market capitalization traded on NASDAQ Stock Market. The NASDAQ 100 Index includes publicly-traded companies from most sectors in the global economy, the major exception being financial services.

A diversified portfolio does not assure a profit or protect against loss in a declining market.

Compliance Case # 7594817.1._020325_C

{kind=link}